[LATEST] Decree 320/2025/ND-CP Guiding the Implementation of the 2025 Corporate Income Tax Law

GTG CRM Team · GTG CRM

December 20, 2025

![[LATEST] Decree 320/2025/ND-CP Guiding the Implementation of the 2025 Corporate Income Tax Law](https://assets.gtgcrm.com/gtgcrm-home-page/huong-dan-thi-hanh-luat-thue-thu-nhap-doanh-nghiep/huong-dan-thi-hanh-luạt-thue-doanh-nghiep.png)

Table of Contents

The government has officially issued Decree 320/2025/ND-CP, a document detailing and guiding the implementation of the Corporate Income Tax Law of 2025. This decree clarifies how to determine taxable income, the tax calculation method, the tax rates, and corporate income tax incentives.

This is an important legal basis that directly affects the tax declaration and settlement activities of businesses from the 2025 tax year onwards. Therefore, organizations and business households converting to enterprises, as well as existing businesses, need to proactively update their information to apply the regulations correctly and minimize tax risks.

Overview of Decree 320/2025/ND-CP

On December 15, 2025, the Government issued Decree 320/2025/ND-CP to provide detailed regulations on certain articles and organizational measures for the implementation of the Corporate Income Tax Law.

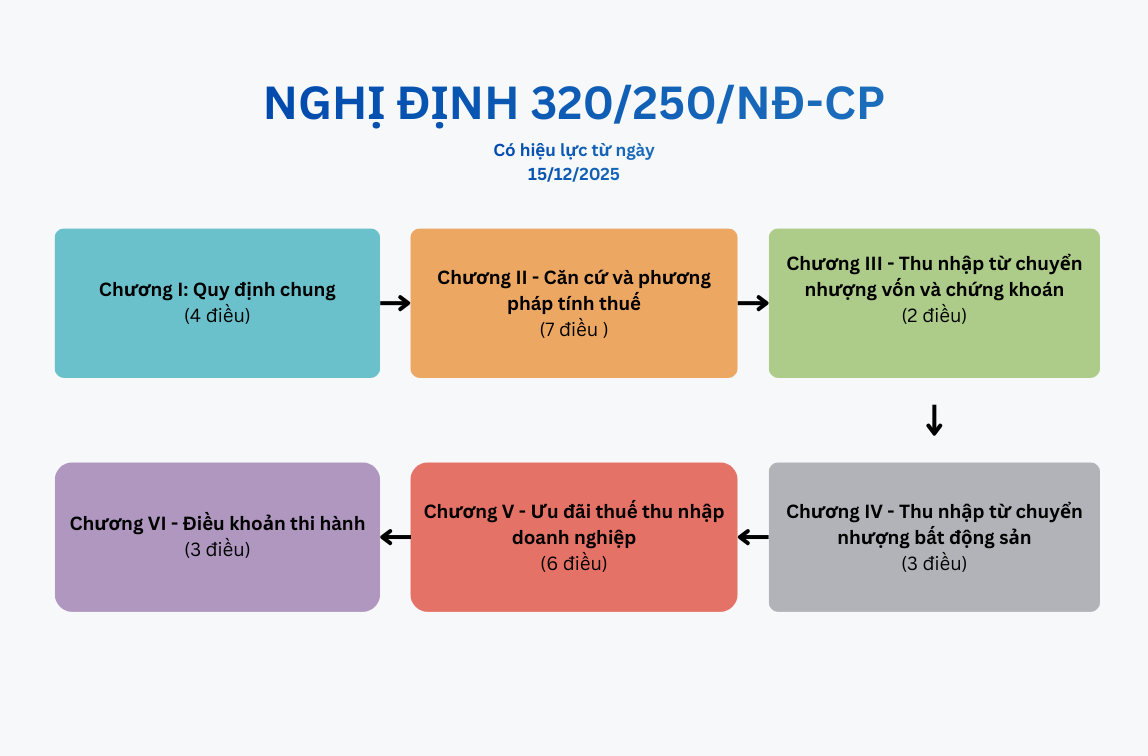

The decree consists of 6 chapters and 26 articles, with the following specific contents:

The full content of Decree 320/2035/ND-CP

Chapter I - General Provisions

It consists of 4 articles (Articles 1 to 4)

Chapter II - Basis and methods for calculating tax

It consists of 7 articles (Articles 5 to 12)

Chapter III - Income from the transfer of capital and securities

It consists of 2 articles (Article 13, Article 14)

Chapter IV - Income from the transfer of real estate

It consists of 3 articles (Articles 15 to 17)

Chapter V - Corporate Income Tax Incentives

It consists of 6 articles (Articles 18 to 23)

Chapter VI - Enforcement Provisions

It consists of 3 articles (Articles 24 to 26)

View the full text of Decree 320/2025/ND-CP

Scope of regulation and subjects of application

The Decree provides detailed regulations for the implementation of the Corporate Income Tax Law, including:

- Determining taxable income

- Tax basis

- Tax rate

- Tax calculation method

- Principles and conditions for enjoying tax incentives

The regulations apply to organizations and individuals involved in the above-mentioned matters.

Corporate income tax payers include:

- The business is established and operates in accordance with Vietnamese law.

- Foreign businesses with or without a permanent establishment in Vietnam

- Public service units, cooperatives, cooperative unions

- Credit institutions and other economic organizations that generate taxable income.

Determining taxable corporate income

How to determine taxable corporate income

Taxable income for corporate income tax

According to Decree 320/2025/ND-CP, taxable corporate income includes:

- Income from the production and sale of goods and services.

- Other income as prescribed by tax law.

The "other income" category is quite broad, including but not limited to:

- Income from capital gains and securities transfers

- Income from the transfer of real estate and investment projects

- Income from ownership and use of property

- Income from renting property

- Income from the liquidation and transfer of assets (excluding real estate)

- Interest on deposits, interest on loans

- Exchange rate difference

- Bad debts that were written off but recovered

- Gifts, presents, and other income as stipulated by regulations.

Businesses need to properly classify these income streams in order to fully declare them when determining taxable income.

Income exempt from corporate income tax.

In addition to taxable income, the Decree also clearly specifies tax-exempt income, including:

- Income from fishing activities

- Income from agricultural, forestry, and fisheries production, especially in areas with difficult socio-economic conditions.

- Income from technical services directly serving agriculture.

- Income from contracts for scientific research, technological development, innovation, and digital transformation (exempt from tax for 3 years)

- Income from business operations employing people with disabilities, people recovering from drug addiction, and people infected with HIV/AIDS.

Basis and methods for calculating corporate income tax.

Basis for tax calculation:

Corporate income tax is determined based on:

- Taxable income for the period

- Corresponding corporate income tax rates

Principles of profit and loss offsetting and loss carryforward:

Businesses are allowed to offset profits and losses between production and business activities within the same tax period. However, please note:

- Losses from the transfer of real estate or investment projects cannot be offset against income from operations enjoying tax incentives.

- The loss is carried forward entirely and continuously to subsequent years, for a maximum of 5 years.

Revenue subject to tax

Revenue for calculating taxable income is the total amount of money a business receives from selling goods, processing services, and providing services, regardless of whether the money has been collected or not.

The decree provides clear guidance:

- Time of revenue recognition

- Methods for determining revenue in specific cases such as:

- Installment sales, deferred payment.

- Property rental

- Construction and installation activities

- Business Cooperation Contract (BCC)

- Other cases as prescribed.

Deductible and Non-Deductible Expenses

Conditions for expenses to be deductible:

An expense must simultaneously meet three conditions to be considered a deductible expense:

- Issues arising from and related to production and business activities.

- We have all the necessary legal invoices and documents.

- Non-cash payment documents are required for transactions of 5 million VND or more.

Non-deductible expenses include:

- The costs do not meet the above conditions.

- Administrative fines

- Excess spending beyond the prescribed limits for employee welfare expenses.

- The interest portion corresponds to the remaining shortfall in registered capital.

Corporate income tax rate

According to Decree 320/2025/ND-CP:

Standard tax rate: 20%

Preferential tax rates based on revenue size:

- 15%: businesses with total annual revenue not exceeding 3 billion VND.

- 17%: businesses with revenue ranging from over 3 billion to no more than 50 billion VND.

Special tax rates:

- 25% to 50% for oil and gas exploration, production, and extraction activities.

- 40% or 50% for the exploitation of rare resources.

Foreign businesses without a permanent establishment in Vietnam are subject to a percentage-based tax on revenue, for example:

- Service fees: 5% (10% for restaurant, hotel, and casino management)

- Royalties: 10%

- Capital transfer: 2%

Corporate income tax incentives

Preferential treatment for industries and geographical areas.

Notable industries and occupations eligible for incentives:

- High-tech applications, R&D

- Software production and IT services

- Supporting industries

- Renewable energy, clean energy

- State investment in key infrastructure

- A large-scale production project with an investment of 12,000 billion VND.

Local discounts apply to:

- Areas with difficult or extremely difficult socio-economic conditions.

- Economic zones, high-tech zones, high-tech agricultural zones, concentrated digital technology zones.

Preferential tax rates

- A tax rate of 10% for 15 years applies to new investment projects in prioritized sectors or located in particularly disadvantaged areas.

- A 10% tax rate throughout the operating period applies to certain sectors including agriculture, socialized services, and social housing.

- A tax rate of 17% for 10 years applies to other preferential projects or those located in disadvantaged areas.

Tax exemptions and reductions

- Exemption from tax for 4 years, and a 50% reduction in tax payable for the following 9 years, as stipulated in Clause 1, Article 19 of the Corporate Income Tax Law.

- Exemption for 2 years, 50% reduction for the following 4 years, as stipulated in Clause 4, Article 19 of the Decree.

- Incentives for expansion investment projects

- Two-year tax exemption for newly established businesses converted from household businesses.

- Additional incentives for costs for female workers and ethnic minority workers.

Effective date

Decree 320/2025/ND-CP takes effect from December 15, 2025 and applies to the corporate income tax period of 2025.

Businesses can choose to apply regulations regarding revenue, expenses, tax incentives, tax exemptions and reductions, and loss carryforward according to one of the following thresholds:

From the beginning of the 2025 tax year

- From the date the Corporate Income Tax Law came into effect

- From the date the Decree comes into effect

Certain specific regulations, such as cashless payments and capital transfers, will apply from the date the Decree takes effect.

Summary

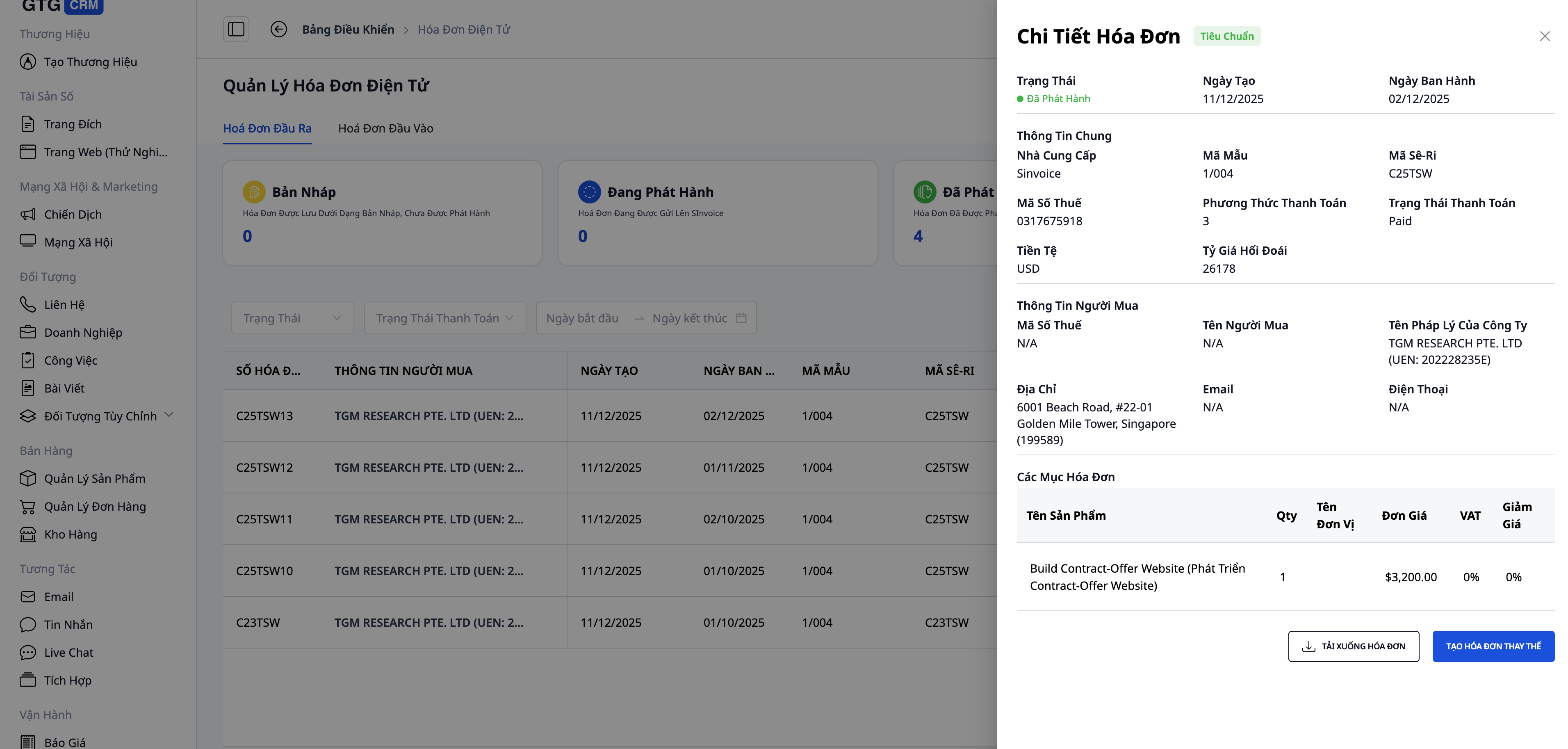

Decree 320/2025/ND-CP sets higher requirements for transparency in revenue and tax obligations, especially for small businesses and household businesses. Proactively monitoring revenue, issuing complete invoices, and centrally storing data not only helps comply with regulations but also contributes to rationalizing lump-sum tax rates and reducing the risk of inaccurate tax assessments. With sales, revenue, and invoice management tools integrated into GTG CRM, businesses can effectively control business data from the outset, support more transparent work with tax authorities, and create a sustainable operational foundation in line with the spirit of Decree 320/2025/ND-CP. Key features include:

- Create and manage electronic invoices directly from transaction data.

- Automatically fill in customer information, reducing errors that occur when entering data manually.

- Track invoice status (issued, sent, paid).

- Centralized invoice storage makes it easy to search and reconcile invoices when needed.

- Connecting with leading electronic invoicing providers such as Sinvoce, Misa, etc., helps businesses comply with current legal regulations.

Illustrating an invoice created using GTG CRM

Turn what you've just read into tangible results — apply it now with GTG CRM, free.

Apply nowMaybe You Should Read These

Case Study: Ms. Lan Anh - From Multichannel Management Confusion to Effective Sales with GTG CRM

Thien Nam Hoa Electronics Supermarket - Applying CRM to Accelerate Retail

Year-End Marketing & Sales Strategies and the Role of GTG CRM in Accelerating Revenue

Unlock Ways to Optimize Online Business Processes for Home Goods Shop Owners

What Do Businesses Need From CRM in the Digital Age? GTG CRM's Optimal Solution for Interaction and Comprehensive Growth

From Toys "R" Us's Failure to the Transformation Path for Traditional Businesses in the Digital Age

5 Retail Predictions for 2025 – When GTG CRM Becomes the “AI Infrastructure” for a Unified Shopping Experience

Optimize Lead Distribution for Course Sales: How GTG CRM's AI Reduces Consultation Time and Costs by 60%

Coolmate - Vietnamese Startup Achieves Revenue Breakthrough with CRM and Automation

Case Study: Temu - When Engagement & Personalization are Key to Growth

Optimize Social Media with AI: Secrets to Boosting Content Performance with Buffer and Hootsuite