Common Invoice Issuance Errors Subject to Penalties: Fines, Statutes of Limitations, and Resolution

GTG CRM Team · GTG CRM

December 20, 2025

Table of Contents

In the tax administration process, invoices are not only ordinary accounting documents but also a direct basis for tax authorities to determine the revenue, expenses, and tax obligations of businesses. In reality, many businesses and household businesses are penalized not for intentional violations, but for issuing invoices at the wrong time, misrepresenting the nature of the transaction, or using invalid invoices.

This article summarizes common invoice issuance errors that are subject to penalties, along with specific fines, statutes of limitations for penalties, and how to handle incorrect invoices, helping businesses proactively avoid legal risks.

Error 1: Invoice issued at the wrong time.

When is it considered issuing an invoice at the wrong time?

Businesses are considered to have issued invoices at the wrong time when the invoices are not issued at the time stipulated by law, including common cases such as:

- Goods have been delivered or services have been completed, but the invoice was issued late.

- Issue invoices before delivery or before completion of services.

- Invoices are recorded in the wrong accounting period, leading to discrepancies in revenue and tax obligations.

- This error is usually discovered when tax authorities compare the actual transaction date with the electronic invoice data.

Penalties for issuing invoices at the wrong time.

Penalties for issuing invoices at the wrong time.

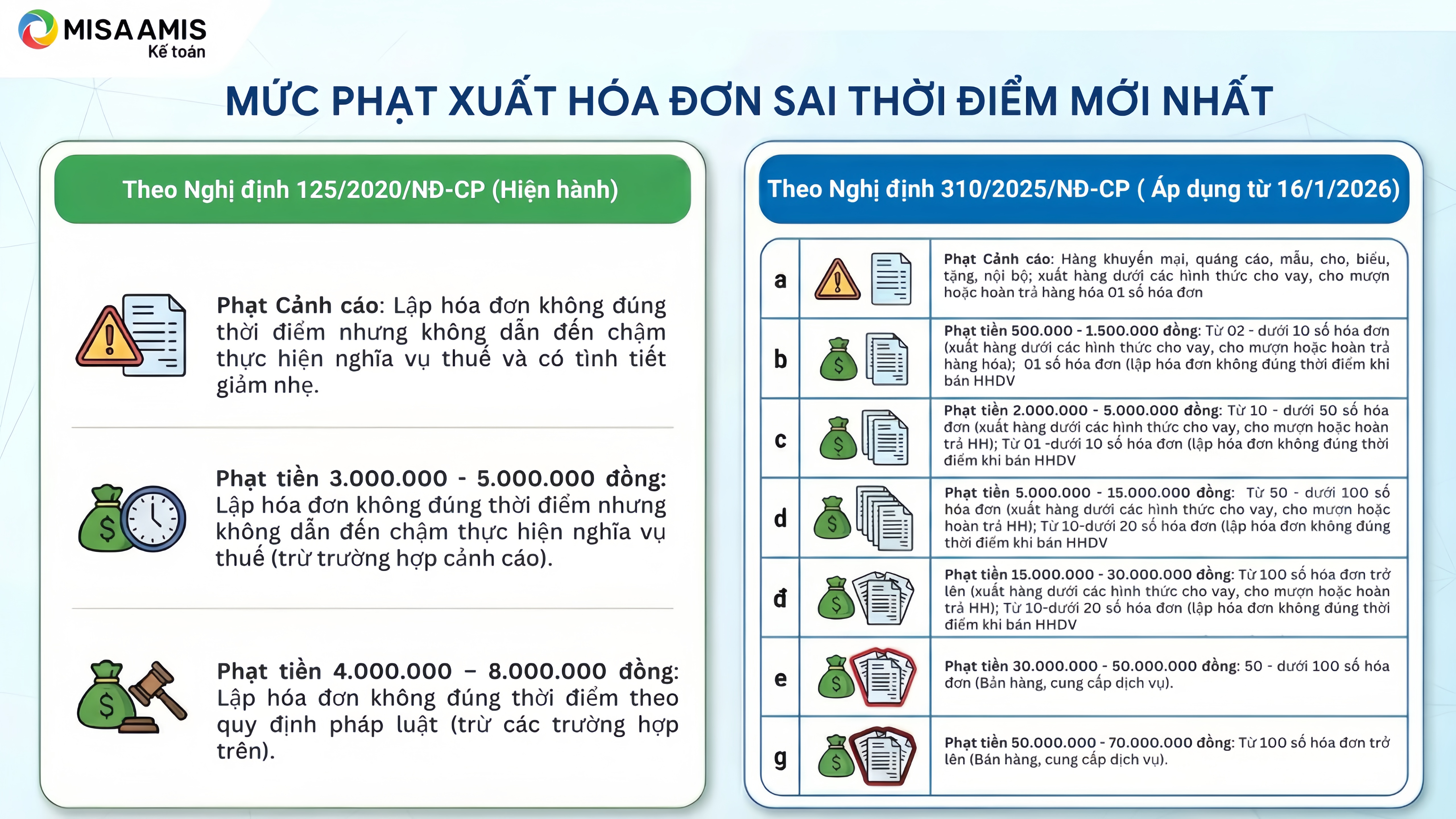

According to Decree 125/2020/ND-CP (applicable until before January 16, 2026)

- Warning: Applies when invoices are issued at the wrong time but do not delay tax obligations and there are mitigating circumstances.

- A fine of VND 3,000,000 to VND 5,000,000 will be applied when invoices are issued at the wrong time but do not result in a delay in tax obligations.

- A fine of VND 4,000,000 to VND 8,000,000 will be applied to the act of issuing invoices at an incorrect time according to regulations on the sale of goods and provision of services.

According to Decree 310/2025/ND-CP (effective from January 16, 2026)

The penalty amount is determined based on the number of invoices that violate the regulations.

- Warning penalty: Promotional items, advertising materials, samples, gifts, donations; internal transactions; goods shipped under the form of loans, borrowings, or returns; issuing invoices with a certain number of invoices.

- Fines of VND 500,000 - VND 1,500,000: From 2 to less than 10 invoices (exporting goods under the form of loans, borrowing, or returning goods); 1 invoice (issuing an invoice at the wrong time when selling goods or services).

- Fines of VND 2,000,000 - VND 5,000,000: From 10 to less than 50 invoices (exporting goods under the form of loans, borrowings, or returns); From 1 to less than 10 invoices (issuing invoices at the wrong time when selling goods or services).

- Fines of VND 5,000,000 - VND 15,000,000: From 50 to under 100 invoices (issuing goods under the form of loans, borrowings, or returns); From 10 to under 20 invoices (issuing invoices at the wrong time when selling goods or services).

- Fines of VND 15,000,000 - VND 30,000,000: For 100 or more invoices (exporting goods under the form of loans, borrowings, or returns); For 10 to under 20 invoices (issuing invoices at the wrong time when selling goods or services).

- Fine of 30,000,000 - 50,000,000 VND: 50 - under 100 invoices (sales, services)

- Fines of 50,000,000 - 70,000,000 VND: For 100 or more invoices (sales, services).

How to handle situations where invoices have been issued at the wrong time.

For the seller

- Re-determine the actual time the transaction occurred.

- VAT declaration and recognition of revenue for corporate income tax purposes should be based on the transaction date, not the invoice date.

- Adjust your tax return if you have filed it for the wrong period.

For the buyer

- Declare input VAT at the time the invoice is received.

- Record deductible expenses for corporate income tax purposes in the period in which the actual transaction occurs.

If an invoice is found to be dated incorrectly, the buyer should request the seller to correct it promptly to avoid the risk of using an invalid invoice.

Example

The invoice was issued on January 1, 2026, but the goods were actually delivered on December 31, 2025:

- The seller recognizes revenue and declares taxes in the December 2025 period.

- The buyer declares VAT in January 2026, but records the expense in 2025.

Error 2: Issuing fictitious invoices or using illegal invoices.

What is a fake invoice?

A fictitious invoice is an invoice that does not accurately reflect the actual economic transaction, including:

- Fraudulent invoices, invoices without actual transactions: Invoices that contain complete information but where goods or services were purchased, did not actually occur, or only partially occurred.

- Incorrectly reflecting the actual value: An invoice that records a value higher or lower than the actual value of the goods or services sold.

- Invoices lacking required information: Invoices that do not fully include the required information such as the name, address, tax code of the seller and buyer, date, description of goods/services, unit of measurement, quantity, unit price, and total amount as stipulated.

- Invoices that have been altered or modified improperly: Invoices that have been altered or modified without complying with regulations on invoice modification.

- The invoice has discrepancies between copies: The values on the different copies of the invoice are different and do not match.

- Using invoices from other organizations or individuals to legitimize transactions: Using invoices that are not from your own business to prove the purchase or sale of goods or services.

- Using invoices that have been deemed illegal by authorities: Invoices that have been concluded by the tax authorities, police, or other authorities to be used illegally.

- The invoice was issued by an organization that is not authorized to issue invoices, or the invoice is not yet valid.

Penalties for issuing fraudulent invoices

Penalties will be imposed for false declarations resulting in a shortfall in tax payable or an increase in tax exemptions, reductions, or refunds.

A penalty of 20% of the amount of underdeclared tax or the amount of tax exempted, reduced, or refunded in excess of regulations will be imposed for using illegal invoices and documents to account for the value of purchased goods and services, thereby reducing the amount of tax payable or increasing the amount of tax refunded, exempted, or reduced, but when discovered by the tax authorities during an inspection, the buyer can prove that the violation of using illegal invoices and documents was the fault of the seller and the buyer has fully accounted for the transaction according to regulations.

Penalties for tax evasion (Article 17 of Decree 125/2020/ND-CP): Depending on the severity of the violation and aggravating/mitigating circumstances, the specific penalties are as follows:

- A fine equal to the amount of tax evaded will be imposed if the offender has one or more mitigating circumstances.

- A fine equal to 1.5 times the amount of tax evaded will be imposed, unless there are aggravating or mitigating circumstances.

- A fine equal to twice the amount of tax evaded will be imposed if there is an aggravating circumstance.

- A fine equal to 2.5 times the amount of tax evaded will be imposed if there are two aggravating circumstances.

- A fine equal to three times the amount of tax evaded will be imposed if there are three or more aggravating circumstances.

In serious cases, individuals and commercial legal entities may be held criminally liable under the Criminal Code.

How to handle situations where invoices appear to be fraudulent.

When you discover that an invoice does not accurately reflect the transaction:

- Stop using that invoice for tax filing.

- Review all contracts, delivery documents, and payment documents.

- Adjust accounting records and tax documents if there have been any accounting errors.

- Proactively work with tax authorities in high-risk situations.

Continuing to use incorrect invoices after detection may be considered a deliberate violation, leading to harsher penalties.

Statute of limitations for penalties related to invoices

According to the legal regulations on administrative penalties in the field of taxation and invoices, the statute of limitations for imposing administrative penalties related to invoices is 2 years.

How to determine the time limit for calculating the statute of limitations:

- With the violation having ended, the statute of limitations begins from the date the violation ceased.

- For ongoing violations, the statute of limitations begins from the date the competent authority discovers the violation.

This means that even after the business has corrected the error, the risk of penalties still exists for up to two years.

Conclude

Invoicing errors, ranging from incorrect timing to fictitious invoices, have clear penalty frameworks and statutes of limitations extending up to two years. In the context of tax administration increasingly relying on electronic data, issuing invoices that do not accurately reflect the nature of the transaction poses significant risks in terms of penalties, tax recovery, and legal liability.

Proactively controlling sales transactions, revenue, and invoicing timing from the outset is a key factor in minimizing risks for businesses. With a centralized management platform like GTG CRM, businesses can track orders, revenue, and invoices on a single system, thereby issuing invoices on time, ensuring transparency in sales data , and supporting the rationalization of tax obligations, especially for small and medium-sized enterprises facing pressure from lump-sum taxes and tax audits.

An illustrative invoice created by GTG CRM

Turn what you've just read into tangible results — apply it now with GTG CRM, free.

Apply nowMaybe You Should Read These

Case Study: Ms. Lan Anh - From Multichannel Management Confusion to Effective Sales with GTG CRM

Thien Nam Hoa Electronics Supermarket - Applying CRM to Accelerate Retail

Unlock Ways to Optimize Online Business Processes for Home Goods Shop Owners

What Do Businesses Need From CRM in the Digital Age? GTG CRM's Optimal Solution for Interaction and Comprehensive Growth

From Toys "R" Us's Failure to the Transformation Path for Traditional Businesses in the Digital Age

Sephora boosts revenue by 142% with automated customer journeys

Year-End Marketing & Sales Strategies and the Role of GTG CRM in Accelerating Revenue

Optimize Lead Distribution for Course Sales: How GTG CRM's AI Reduces Consultation Time and Costs by 60%

CASE STUDY: Increasing Conversion Rate and Optimizing Advertising Costs for Fashion Chain A-Style with GTG CRM

Optimize Social Media with AI: Secrets to Boosting Content Performance with Buffer and Hootsuite

Secrets to Sustainable Online Children's Fashion Business: Increase Revenue with GTG CRM