A sole proprietorship is a form of business organization established and operated by an individual or a group of household members. Due to this characteristic, tax regulations for sole proprietorships differ significantly from those for businesses. Understanding the types of taxes payable and how to fulfill tax obligations will help business owners comply with the law and avoid administrative penalties.

The following article summarizes all the taxes and fees that sole proprietorships need to be aware of, along with detailed guidance on how to declare and pay taxes according to the current regulations of the Ministry of Finance.

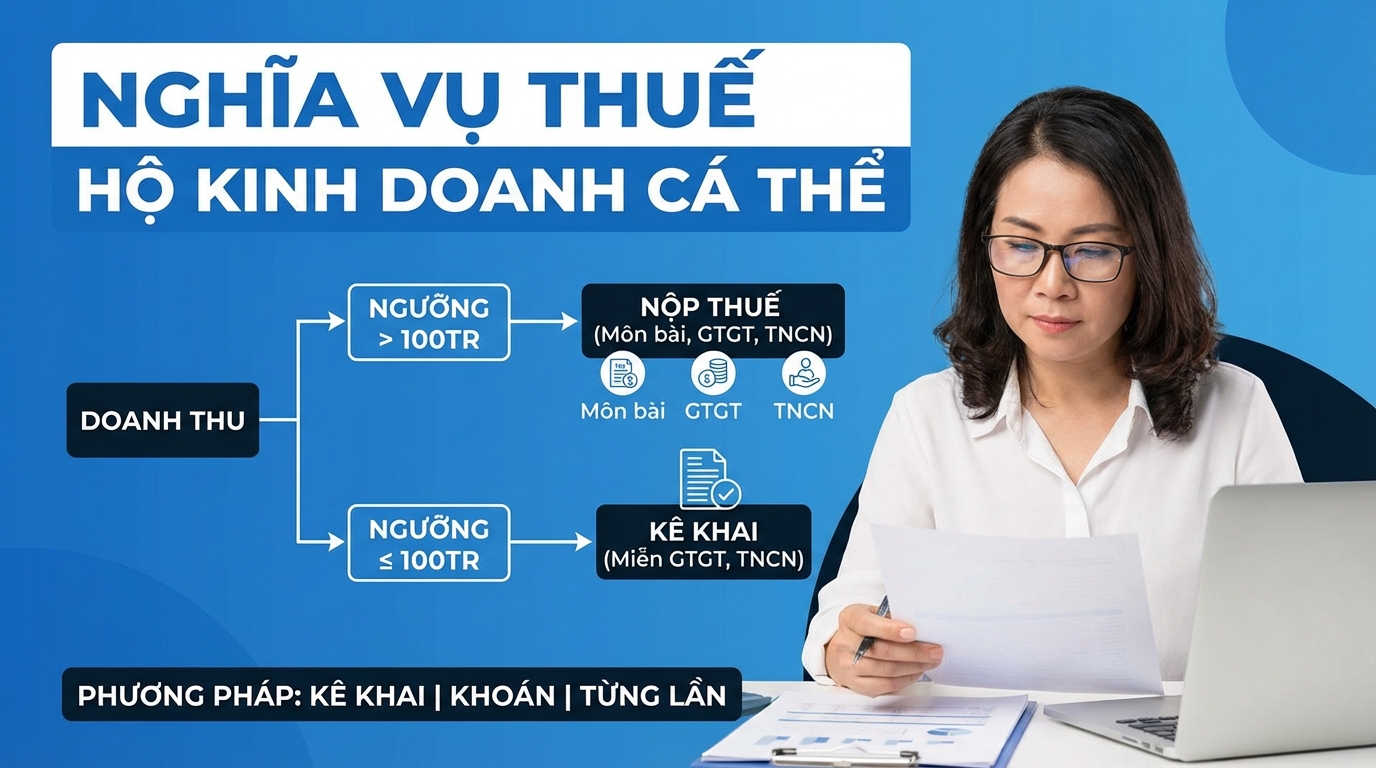

Revenue Threshold for Taxation

According to Circular 40/2021/TT-BTC, sole proprietorships with annual revenue from business activities not exceeding VND 100 million will be exempt from value-added tax (VAT) and personal income tax (PIT). However, even if no tax is payable, sole proprietorships are still responsible for full, accurate, and timely declarations as required.

For sole proprietorships formed by a group of individuals or families, the VND 100 million/year revenue threshold is calculated for the single representative of the group for the tax year, not per individual member.

Taxes and Fees Payable by Sole Proprietorships

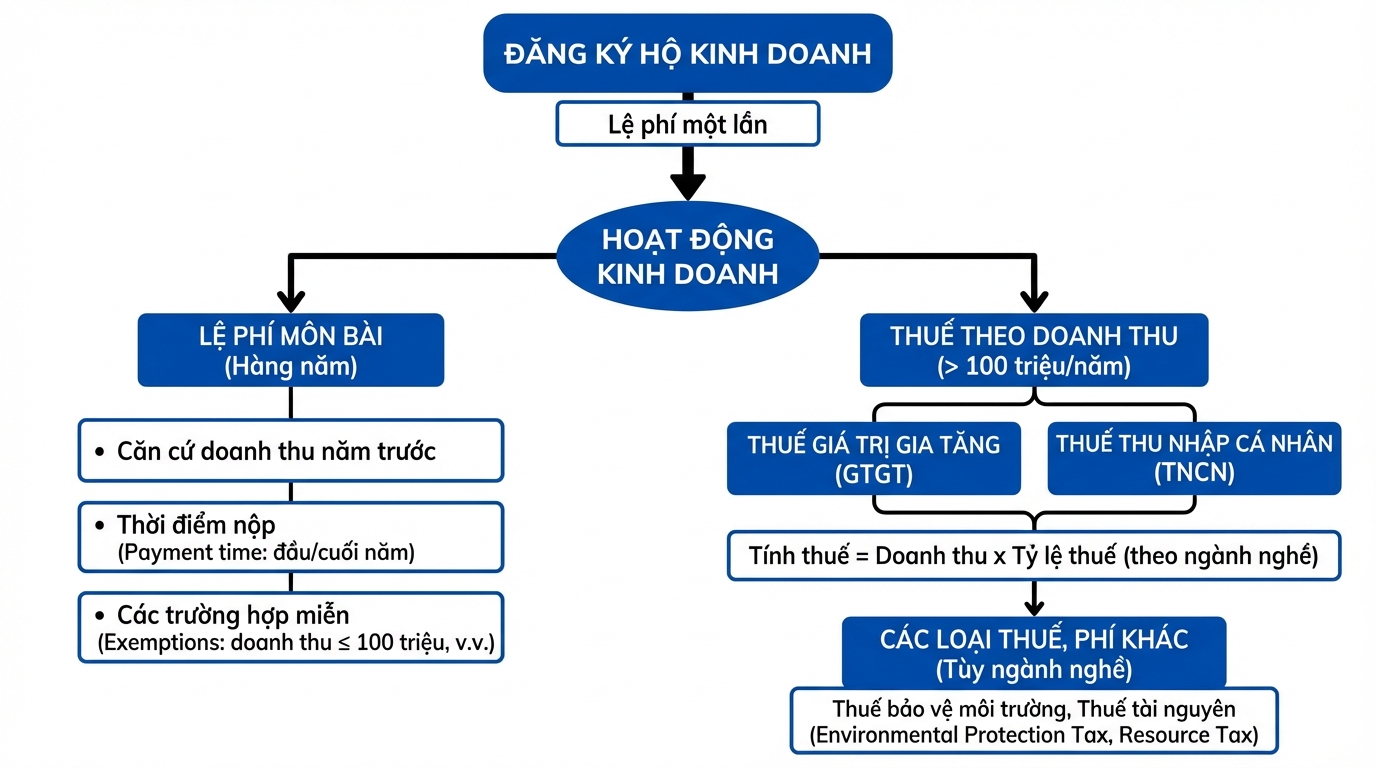

Business Registration Fee

This is a one-time fee paid when registering the establishment of a sole proprietorship with the competent authority. The fee is specified by each locality and is generally not high.

Annual Business License Fee (Lệ phí môn bài)

The annual business license fee is a yearly charge that sole proprietorships must pay, calculated based on the previous year's revenue. According to Circular 65/2020/TT-BTC, the fee varies depending on the revenue scale and is divided into different tiers.

Payment Deadline for Annual Business License Fee:

Sole proprietorships commencing operations in the first six months of the year must pay the full annual fee. If operations begin in the last six months of the year, only 50% of the annual fee is payable.

If a sole proprietorship temporarily suspends operations and submits a written notification to the tax authority or business registration authority before January 30th of each year, and has not yet paid the annual fee for that year, they will be exempt from the fee for the year of suspension.

How to Determine Revenue for Fee Calculation:

Revenue used as a basis for calculating the annual business license fee is the total revenue subject to personal income tax in the preceding year, excluding income from asset leasing. For newly established sole proprietorships or those resuming operations after dissolution, revenue is determined based on the scale of businesses in the same industry and location.

Cases Exempt from Annual Business License Fee:

Sole proprietorships are exempt from the annual business license fee in the following situations: annual revenue of VND 100 million or less; no fixed business location and not operating regularly; engaged in salt production; aquaculture, fishing, or fishery support services; and in the first year of establishment or commencement of business operations.

Value-Added Tax (VAT)

VAT is applicable to sole proprietorships with annual revenue of VND 100 million or more. The tax rate is a percentage of revenue, varying by specific business industry.

VAT Calculation Formula:

VAT Payable = Taxable Revenue × VAT Rate

Taxable revenue includes all income from sales, provision of services, processing, commissions, as well as bonuses, promotions, discounts, support, surcharges, additional charges, and contract violation compensation.

Personal Income Tax (PIT)

Similar to VAT, PIT also applies to sole proprietorships with annual revenue of VND 100 million or more. The PIT rates are detailed by industry in Appendix I issued with Circular 40/2021/TT-BTC.

PIT Calculation Formula:

PIT Payable = Taxable Revenue × PIT Rate

For sole proprietorships operating in multiple fields and industries, taxes must be declared and calculated separately for each field according to the prescribed rates. If revenue for each field cannot be determined or is declared inconsistently with reality, the tax authority will assess it according to tax administration laws.

Other Taxes and Fees

Depending on the specific nature of their business, sole proprietorships may also be liable for other taxes such as environmental protection tax (for fuel and plastic bag businesses), natural resource tax (for natural resource exploitation), or other fees and charges as stipulated by law.

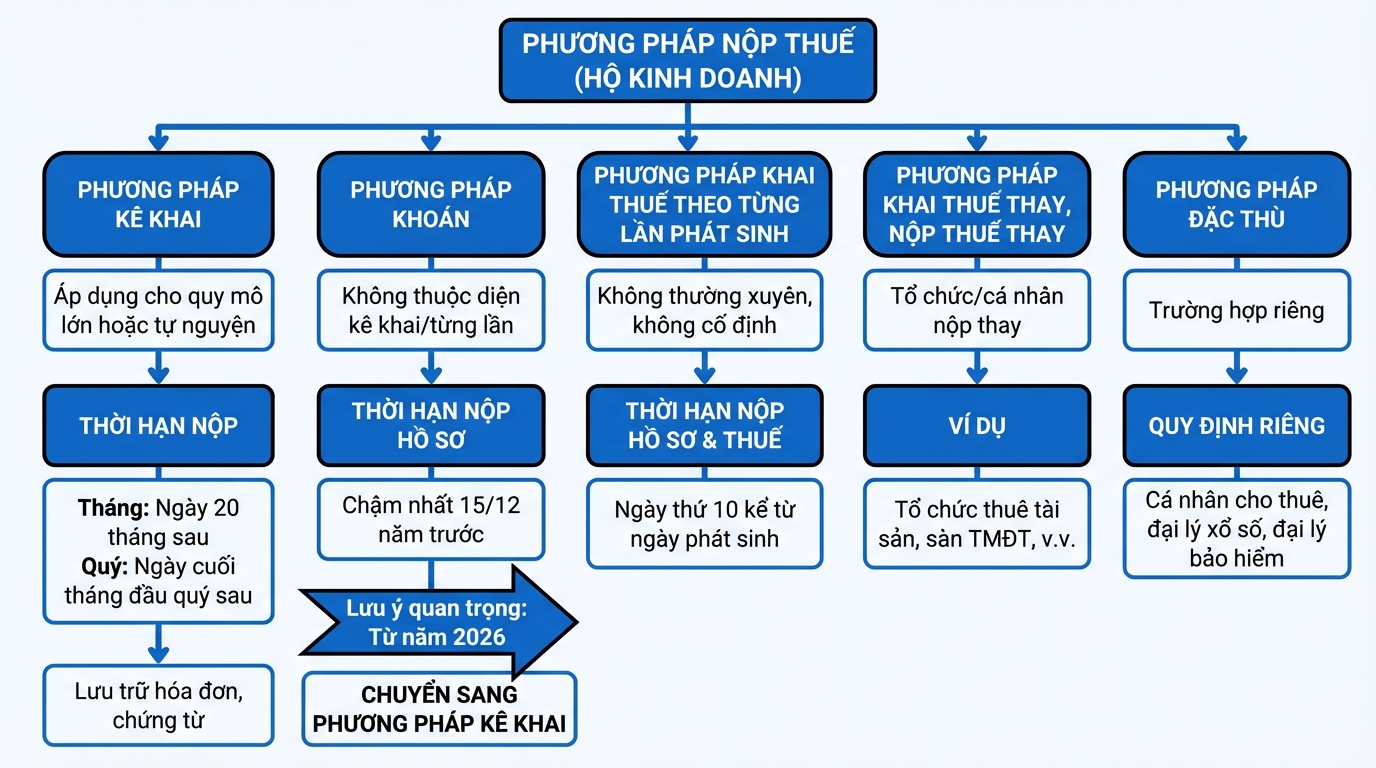

Tax Payment Methods

Sole proprietorships can adopt one of the following tax payment methods, depending on their scale and operational characteristics:

Declaration Method

Applicable to large-scale sole proprietorships or those not meeting large-scale criteria but voluntarily choosing this method.

The deadline for monthly tax declarations is the 20th day of the following month. For quarterly declarations, the deadline is the last day of the first month of the subsequent quarter.

Tax payment deadlines coincide with tax declaration deadlines. Sole proprietorships are not required to maintain full accounting records but must retain invoices, receipts, and contracts to prove the legality of goods and services.

Lump-sum Method (Phương pháp khoán)

Applicable to sole proprietorships not subject to the declaration method or occasional transactions.

The deadline for tax declarations is the 15th day of December of the year preceding the tax year. For newly established businesses, those changing tax calculation methods, or altering industries or scale, the deadline is the 10th day from the date of change.

Important Note: From 2026, in line with the tax sector's digital transformation roadmap, all sole proprietorships will be required to switch from the lump-sum method to the declaration method. This necessitates that sole proprietorships prepare their sales management systems, electronic invoices, and transparent tax declarations.

Declaration Method for Occasional Transactions

Applicable to sole proprietorships that operate infrequently and do not have a fixed business location.

The deadline for tax declarations is the 10th day from the date the tax obligation arises. Tax payment deadlines coincide with tax declaration deadlines.

Tax Declaration and Payment by a Third Party

In certain special cases, organizations or individuals will declare and pay taxes on behalf of sole proprietorships. Examples include organizations leasing assets from individuals, organizations partnering with individuals, organizations paying sales bonuses, and owners of e-commerce platforms.

Specific Methods

Applicable to specific cases such as individuals leasing assets, individuals directly contracting as lottery agents, insurance agents, or multi-level marketing agents. Each case has its own regulations regarding the tax period and deadlines.

Tax Registration Deadline

According to Article 33 of the Law on Tax Administration 2019, sole proprietorships have 10 working days from the date of receiving their business registration certificate to register for tax with the managing tax authority. Timely tax registration is a mandatory requirement to avoid administrative penalties.

Consequences of Late or Non-Tax Declaration

Late submission or failure to submit tax registration documents and tax declarations will result in administrative penalties according to Circular 166/2013/TT-BTC, with fines ranging from a warning to VND 5,000,000, depending on the severity of the violation and the delay period.

Specifically, a delay of 1-10 days in submitting tax declarations may incur a fine of VND 700,000; 10-20 days, VND 1,400,000; 20-30 days, VND 2,100,000; 30-40 days, VND 2,800,000; and over 40 days, VND 3,500,000. In addition, sole proprietorships will also be subject to late payment interest calculated on the overdue tax amount as stipulated.

Conclusion

A thorough understanding of tax regulations not only helps sole proprietorships comply with the law but also lays a solid foundation for sustainable development in an increasingly professionalized business environment.

Turn what you've just read into real results — apply it now with GTG CRM, free.

Apply Now