The Ministry of Finance recently proposed tax exemption for businesses with annual revenue under 500 million VND, expected to take effect from July 1, 2026. This information is of great interest to many businesses, promising to significantly reduce the tax burden and create conditions for small businesses to develop more stably.

Raising the tax exemption threshold from 200 million to 500 million VND per year is considered an important step in supporting the individual economic sector. It is estimated that about 90% of current businesses will no longer have to pay taxes, allowing them to confidently maintain operations and reinvest amidst a volatile market.

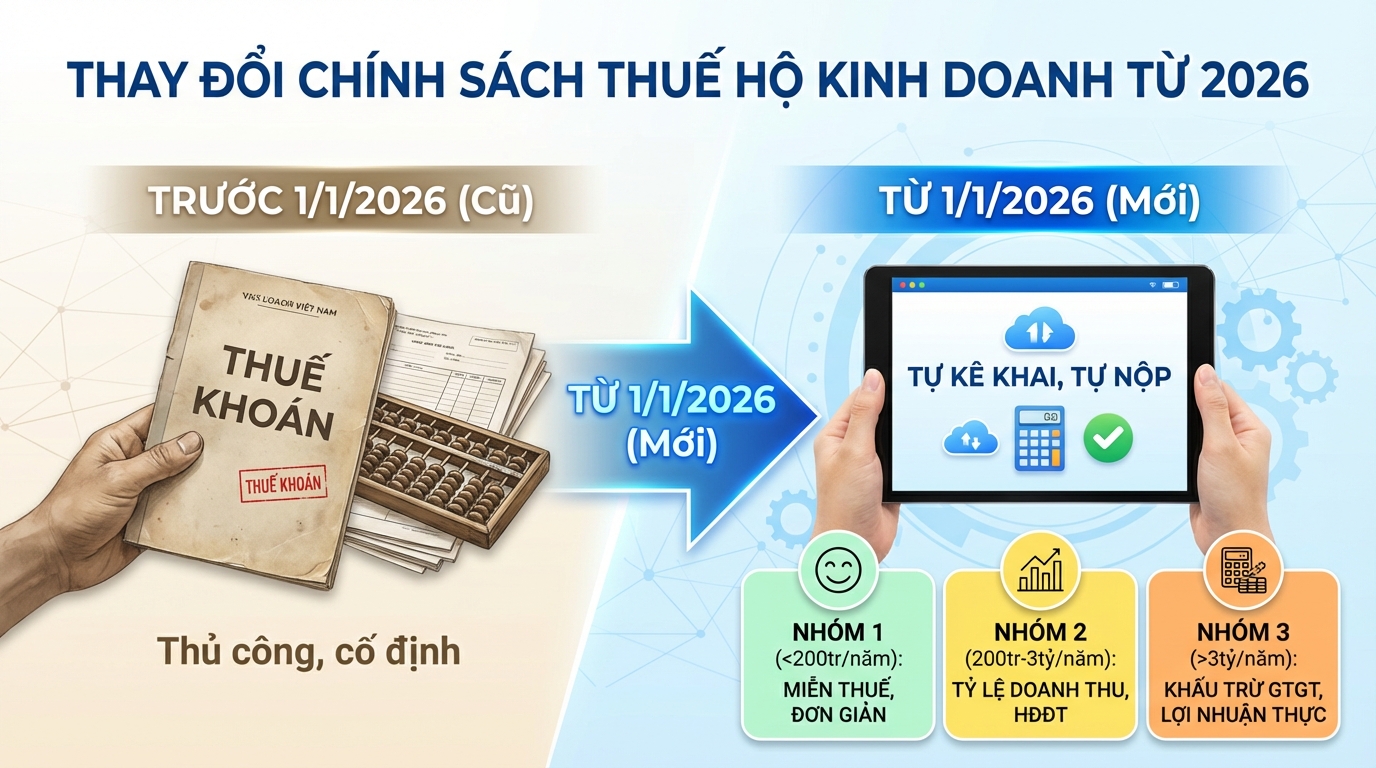

Current Regulations on Taxes for Businesses

According to Decision 3389/QD-BTC in 2025, from January 1, 2026, the method of collecting lump-sum tax for businesses will be completely abolished and replaced with a self-declaration, self-payment management method. Businesses will be divided into 3 main groups:

Group 1: Annual Revenue under 200 million VND

- Exempt from VAT and Personal Income Tax.

- No complex accounting records are required.

- Declaration twice a year, at the beginning and middle/end of the year.

Group 2: Annual Revenue from 200 million to under 3 billion VND

- Apply the direct tax calculation method on revenue.

- Tax rates by industry:

- 1% for distribution and supply of goods.

- 5% for services, construction without material contracting.

- 3% for production, transportation, services related to goods, construction with material contracting.

- 2% for other business activities.

- Tax declaration 4 times a year (quarterly).

- Businesses with annual revenue over 1 billion VND in the retail or direct service sector must issue electronic invoices from a point-of-sale system connected to the tax authority.

Group 3: Annual Revenue over 3 billion VND

- Apply the VAT deduction method: VAT payable = Output VAT – Input VAT.

- Personal Income Tax: 17% on total profit (Profit = Revenue – Reasonable expenses).

- Monthly declaration if revenue is over 50 billion VND/year, quarterly if under 50 billion VND/year.

New Proposal from the Ministry of Finance

On November 27, 2025, the Ministry of Finance issued Official Letter 18491/BTC-CST with the following notable points:

Increase the tax-exempt revenue threshold to 500 million VND/year

- Adjustment from 200 million to 500 million VND/year.

- Approximately 2.3 million households (90% of the total 2.54 million businesses) will be tax-exempt.

- If approved, it will take effect from July 1, 2026.

Tax calculation based on actual income for businesses with revenue over 500 million VND

Businesses and individuals with revenue from 500 million to 3 billion VND/year:

- Tax calculated based on actual income (revenue – expenses).

- Apply a tax rate of 15%, similar to micro-enterprises.

- If expenses cannot be determined, tax will be applied as a percentage of revenue.

Detailed Tax Schedule According to the New Draft

Tax based on income (revenue – expenses):

| Annual Revenue | Tax Rate |

|---|---|

| Over 500 million – 3 billion | 15% |

| Over 3 – 50 billion | 17% |

| Over 50 billion | 20% |

Tax as a percentage of revenue (when expenses cannot be determined):

| Industry | Tax Rate |

|---|---|

| Distribution, supply of goods | 0.5% |

| Services, construction without raw material contracting | 2% |

| Property rental, insurance brokerage, lottery, multi-level marketing | 5% |

| Production, transportation, construction with raw material contracting | 1.5% |

| Digital content products/services | 5% |

| Other industries | 1% |

Specific Regulations for Real Estate Rental

Individuals renting out real estate irregularly (excluding accommodation business) with annual revenue over 500 million VND:

- Only the method of calculating tax as a percentage of revenue applies.

- No need to determine expenses, offset income, or finalize annual tax returns.

Benefits of the New Policy

Reduced Financial Burden for the Majority of Businesses

With 90% of businesses being completely tax-exempt, those with small or unstable revenues can confidently maintain operations, reinvest, and recover better.

Fairer Taxation Based on Actual Income

Businesses with revenue over 500 million VND will have their taxes calculated based on actual profit: those with profit pay taxes, low profit means less or no tax. This is particularly beneficial for businesses with high input costs.

Facilitating Stable Development

The new policy helps small businesses stabilize their livelihoods, enhance competitiveness, and contribute more positively to the economy. This is an important step in supporting the individual economic sector.

Encouraging Transparency and Declaration

Businesses are more motivated to declare and be transparent about their revenue, leading to more effective tax management and easier access to government support and policies.

The Most Obvious Beneficiaries

Small-Scale Businesses

Small grocery stores, eateries, coffee shops, service shops, and small online sellers with annual revenue under 500 million VND will be completely tax-exempt.

Freelance Individuals

Small-scale startups, online sellers, and seasonal sellers with unstable revenue will benefit from the higher tax exemption, helping them to stabilize more confidently.

Businesses with Annual Revenue of 500 million – 3 billion VND

If they can track reasonable expenses, they will have their taxes calculated based on actual income instead of revenue, which is advantageous for businesses with high input costs (inventory, rent, labor...).

Small Retail and Wholesale Industries

Industries where input costs and operating expenses account for a large portion of revenue will benefit from tax calculations based on profit, leading to fairer tax obligations.

Prepare for the Change with GTG CRM

With the transition from lump-sum tax to self-declaration and the proposed increase in the tax exemption threshold, businesses need to prepare clear sales and accounting management systems to accurately track revenue and expenses.

GTG CRM is a multi-channel sales management solution that helps shop owners and businesses:

- Automatically synchronize orders from multiple e-commerce platforms (Shopee, Lazada, TikTok Shop, Facebook...).

- Manage revenue, expenses, and profits in real-time.

- Issue detailed revenue reports by day, month, quarter, and year to support tax declarations.

- Transparently manage inventory and goods inflow/outflow.

- Integrate with electronic invoices, helping to meet the invoicing requirements for businesses with annual revenue over 1 billion VND.

With GTG CRM, tracking revenue and expenses becomes simple, helping you easily determine your tax liability according to new regulations and maximize the benefits of the tax exemption policy. Be ready to embrace the changes from July 1, 2026.

Turn what you've just read into real results — apply it now with GTG CRM, for free.

Apply Now