Effective from July 1, 2022, according to the provisions of Decree 123/2020/ND-CP and Circular 78/2021/TT-BTC, business households and individual business persons applying the tax declaration method are obligated to switch to electronic invoices. This is not only a legal requirement but also a significant step in modernizing business operations.

To ensure compliance with regulations and avoid legal risks, business household owners need to thoroughly understand the rules related to creating, using, and managing electronic invoices. This article will clarify the key points to help you operate your invoicing business accurately and effectively.

Concept of Electronic Invoices

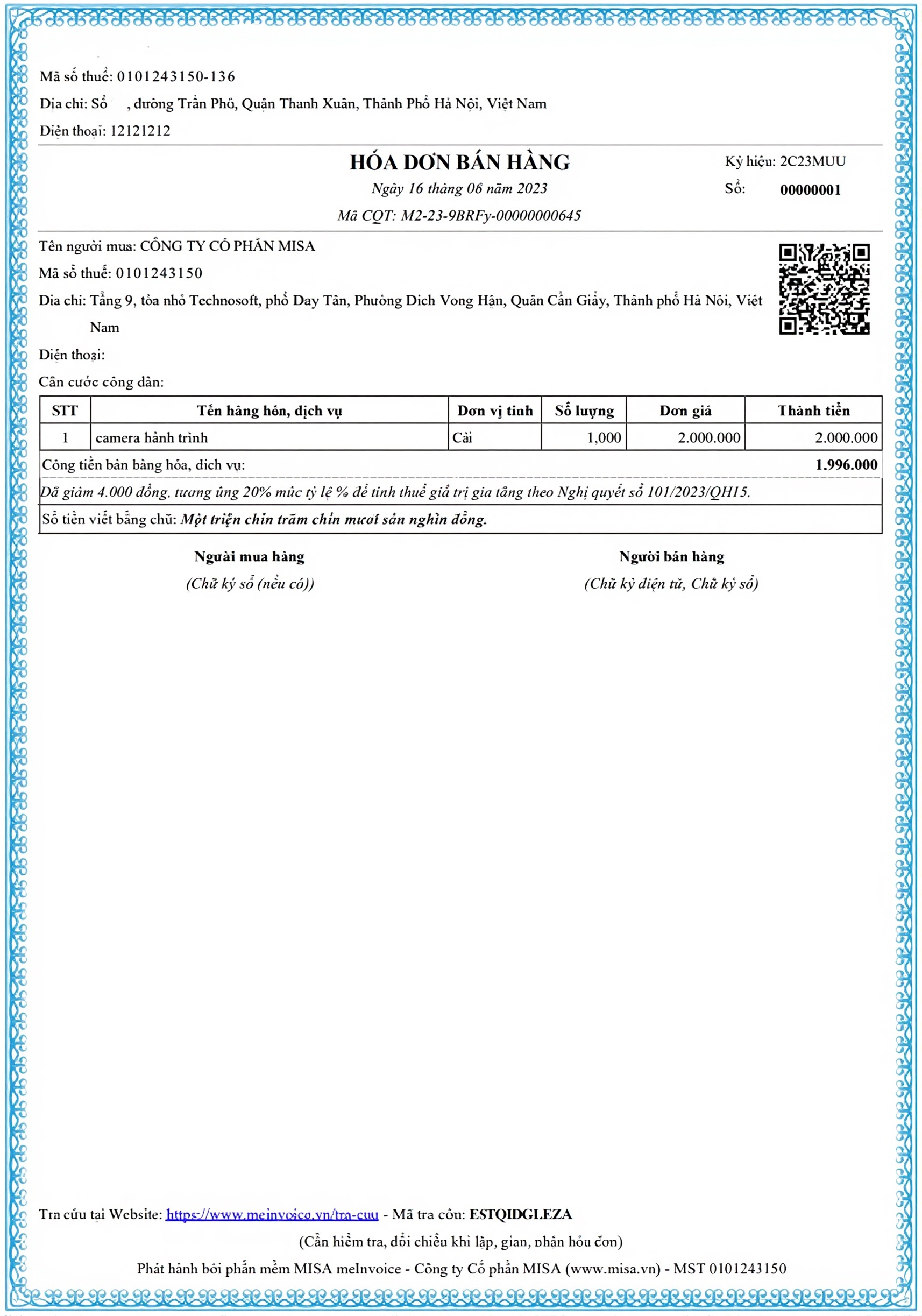

According to Article 3 of Decree 123/2020/ND-CP, an electronic invoice is a document in electronic data format created by the seller of goods or services through electronic means, for the purpose of recording commercial transaction information in accordance with the law on accounting and tax. This invoice can be generated from a cash register connected directly to the tax authority's system.

Electronic invoices are divided into two main types. The first type is an invoice with a tax authority code, which is assigned a code before being sent to the buyer. This code includes a unique transaction number and an encrypted character string based on the seller's information. The second type is an invoice without a tax authority code, which is self-created by the organization and sent directly to the customer without prior authentication from the tax authority.

Three Cases Requiring Electronic Invoice Usage

According to Circular 78/2021/TT-BTC, business households and individual business persons must use electronic invoices in three specific situations.

The first case applies to business households and individuals paying taxes using the declaration method. This group is obligated to use electronic invoices regularly in their business operations.

The second case relates to business households paying taxes using the lump-sum method. When they need to issue an invoice, they will be issued an electronic invoice with a tax authority code for each transaction occurrence.

The third case is for business households declaring taxes on a per-transaction basis. Similar to the second group, if an invoice is requested, the tax authority will issue an individual electronic invoice for each specific transaction.

Key Points to Note When Using Electronic Invoices

Entities Eligible for Per-Transaction Electronic Invoice Issuance

Business households paying taxes using the lump-sum method are supported by the tax authority in issuing coded invoices on a per-transaction basis when needed. Individual business persons who operate irregularly and do not have a fixed business location, and pay taxes on a per-transaction basis, also fall into this category.

Additionally, some special cases are also eligible for per-transaction invoice issuance. For example, business households that have ceased operations but have not yet completed the tax code termination procedures can still apply for invoices to liquidate assets. Business households temporarily suspending operations but needing to complete previously signed contracts will receive similar support. Cases where operations are forcibly suspended due to invoice usage violations are also included in this list.

Electronic Invoice Service Fee Exemption

According to Clause 1, Article 14 of Decree 123/2020/ND-CP, small and medium-sized enterprises, cooperatives, business households, and individual business persons in areas with difficult or especially difficult socio-economic conditions are exempt from the fee for coded electronic invoice services for 12 months from the date of commencement of use. The list of preferential areas is specified in Decree 118/2015/ND-CP.

Entities not eligible for exemption will be required to pay service fees according to the contract signed with the electronic invoice service provider.

Situations Requiring Suspension of Electronic Invoice Usage

Clause 1, Article 16 of Decree 123/2020/ND-CP lists the cases where the use of coded electronic invoices must be suspended.

When a business household terminates its tax code or is verified by the tax authority as not operating at its registered address, the use of invoices will be suspended. Cases where a business household proactively notifies the competent authority of a temporary business suspension also result in the suspension of electronic invoice usage.

Serious violations also lead to similar consequences. If a business household uses invoices to sell smuggled goods, prohibited items, counterfeit goods, or goods infringing intellectual property rights, the authorities will detect and inform the tax authority for processing. The act of issuing fictitious invoices to embezzle money is also a reason for suspending the use of electronic invoices.

Furthermore, when the tax authority notifies the suspension of invoice usage to enforce tax debt collection, or when the business registration authority requires a temporary suspension of business in conditional sectors due to insufficient standards, business households must also suspend the use of electronic invoices.

Which Tax Authority Issues Per-Transaction Invoices?

Point c, Clause 2, Article 13 of Decree 123/2020/ND-CP clearly stipulates the location for submitting applications for invoice issuance.

For business households and individual business persons with fixed business locations, the application will be submitted to the Tax Department managing the area where business activities are conducted. Conversely, business households and individuals without fixed business locations will submit their applications to the Tax Department of their place of residence or business registration.

Roadmap for Transitioning from Lump-Sum Tax to Declaration Method

Starting from 2026, the tax authority will implement a roadmap to transition business households from the lump-sum tax payment method to the declaration method. This requires business households to fully perform tasks such as bookkeeping, creating and submitting electronic invoices, and declaring and paying taxes online as regulated, instead of simply paying lump-sum taxes as before.

To support small business households in adapting to the new regulations without hiring accountants or undertaking complex manual tasks, many comprehensive digital transformation solutions have been developed, integrating features for sales management, tax declaration, tax payment, electronic invoice issuance, and accounting ledger management on a single platform.

Conclusion

The use of electronic invoices has become a mandatory obligation for business households and individual business persons paying taxes using the declaration method. Understanding the regulations on electronic invoices, from their concept and applicable subjects to cases eligible for issuance and situations requiring suspension, is essential for all business household owners to operate their businesses transparently and in compliance with the law.

Specifically, in the context of transitioning from lump-sum tax to declaration, equipping oneself with suitable tools for managing ledgers, declaring taxes, and issuing electronic invoices becomes more critical than ever. GTG CRM provides integrated automatic electronic invoice issuance functionality, enabling business households to easily issue legal invoices, submit data to the tax authority in accordance with regulations, and also supports checking and detecting errors in input invoices. As a result, owners not only save time but also ensure accuracy in accounting work and full compliance with all operations as required by the tax authority.

Turn what you've read into real results — apply it now with GTG CRM, for free.

Apply now